NRI Tax Implications on Property

NRI Tax Implications on Property: Complete 2026 Guide with Practical Insights for Safe Buying and Selling in India

Hey friend, as an NRI planning to buy or sell property back home in India, tax rules can feel like a maze — especially with distance, currency conversion, and compliance deadlines adding pressure. After guiding hundreds of NRIs from the US, UK, UAE, Canada, Australia, and Singapore on property matters, I can tell you this: understanding NRI tax implications clearly saves you lakhs in overpaid taxes, penalties, and delays while ensuring smooth repatriation of your hard-earned money.

In 2026, the rules remain largely stable after major changes in Budget 2024 (LTCG rate rationalization) and simplifications introduced in Budget 2026. No direct income tax hits you at the time of buying property as an NRI, but stamp duty, registration charges, and GST (on under-construction) apply just like for residents. The real tax action kicks in with rental income and especially when you sell. Let me break down every key NRI tax implication in simple, practical language with real-life examples so you can plan confidently.

No Direct Tax on Purchase – But Budget for Indirect Costs in NRI Tax Implications

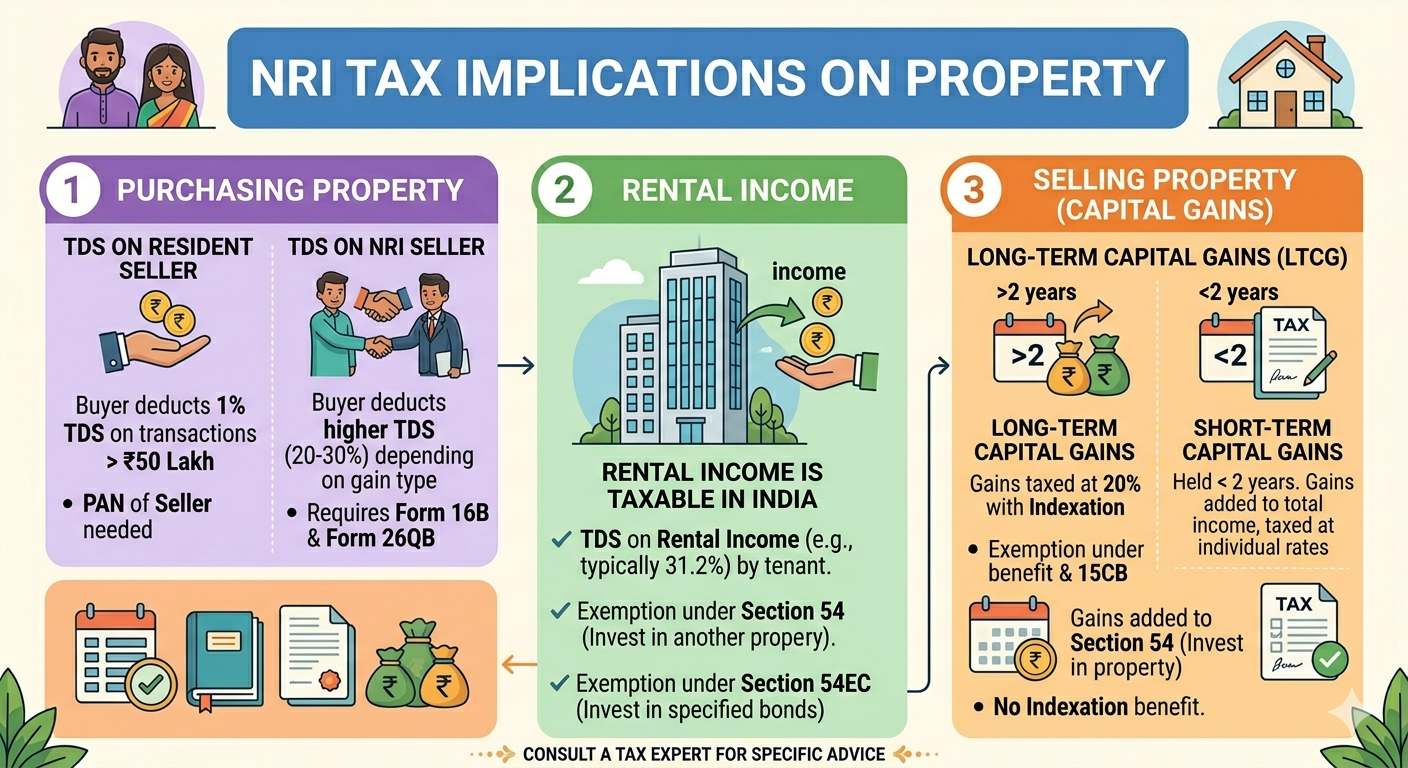

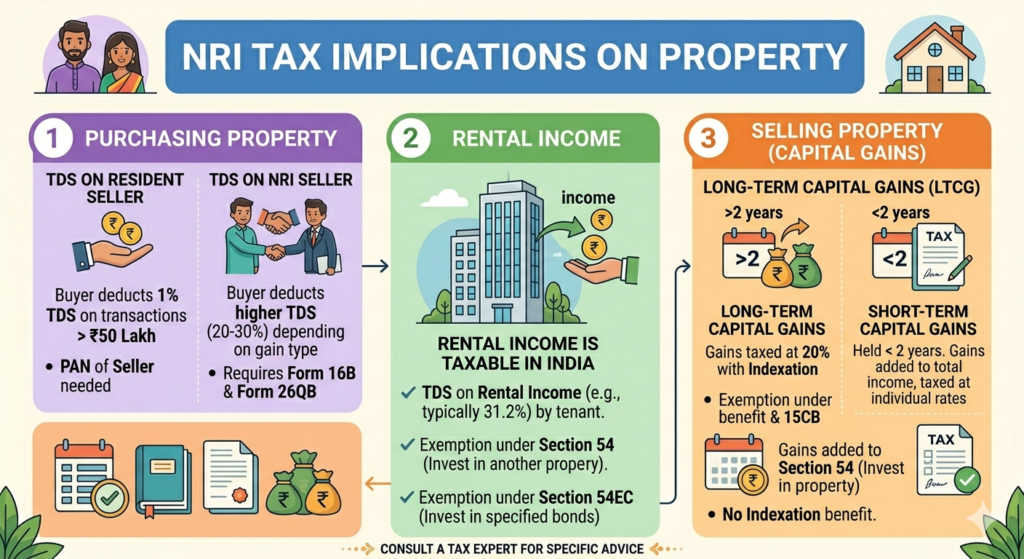

When you buy property in India as an NRI, there is no income tax on the purchase itself. However, you must pay stamp duty (typically 5-8% depending on state and gender/ownership type), registration fees (1-2%), and GST at 5% or 12% on under-construction properties. Funds must come only through proper banking channels — NRE, NRO, FCNR accounts, or inward remittances — to stay FEMA compliant.

In one case I handled for a software engineer in the US, he transferred funds casually without documenting the source properly. When he later wanted to sell, repatriation became complicated because the bank questioned the original inward remittance. Proper documentation at purchase stage is a must in your NRI tax implications planning. Always keep bank statements, SWIFT messages, and FIRC (Foreign Inward Remittance Certificate) ready.

Rental Income – Key Ongoing NRI Tax Implications You Cannot Ignore

Rental income from Indian property is taxable in India for NRIs at slab rates after allowable deductions (standard 30% deduction for repairs/maintenance, municipal taxes, home loan interest, etc.). Tenants must deduct TDS at 30% + cess (around 31.2%) on the rent paid to you under Section 195.

A client from Dubai owning a flat in Bangalore received ₹50,000 monthly rent. The tenant deducted 30% TDS, so my client got only ₹35,000 net. Because India has DTAA with UAE, we claimed a lower effective rate and filed ITR to get a refund of excess TDS. This shows how DTAA helps in NRI tax implications — you can reduce withholding tax by submitting Form 10F and Tax Residency Certificate (TRC) from your country of residence to the tenant or payer.

Always file your Indian Income Tax Return (ITR) even if TDS covers the liability — it helps claim refunds and keeps your records clean for future sales or loans.

Selling Property – Capital Gains and TDS under NRI Tax Implications

This is where most NRI tax implications become critical. When you sell, the buyer deducts TDS on the full sale consideration (not just the gain):

- Short-term capital gains (property held ≤24 months): TDS at 30% + surcharge + 4% cess.

- Long-term capital gains (held >24 months): TDS at 12.5% (post Budget 2024 changes) + surcharge + cess on the full sale value.

Note: For properties acquired before July 23, 2024, some indexation benefits may still apply depending on your choice of regime, but NRIs often do not get the same flexibility as residents in certain old-vs-new calculations. Always compute both options with a tax advisor.

Real-life example: An NRI doctor in Canada sold his inherited flat in Mumbai (held for 5 years) for ₹2.5 crore. The buyer deducted TDS at approximately 12.5% + cess on the entire amount (around ₹31-35 lakhs depending on surcharge). My client’s actual long-term capital gain after cost of acquisition was only ₹80 lakhs. He filed ITR, claimed exemptions under Section 54 (reinvesting in another residential house) or 54EC (bonds), and got a significant refund. Without proper planning, he would have lost that money as blocked TDS.

Budget 2026 Simplification – Big Relief in NRI Tax Implications for Buyers from NRIs

A welcome change in Budget 2026 (effective October 1, 2026): Resident buyers purchasing property from an NRI no longer need to obtain a separate TAN. They can deduct and deposit TDS using their own PAN-based challan. This reduces compliance burden for one-time buyers and speeds up transactions. TDS rates themselves remain unchanged — the simplification is only in the process.

This change directly eases NRI tax implications when you sell, as buyers face less hassle and are more willing to transact with NRIs.

Repatriation of Sale Proceeds – Crucial FEMA Angle in NRI Tax Implications

After paying taxes, you can repatriate the funds abroad, but FEMA rules apply:

- If the property was bought with foreign remittances (NRE/FCNR or inward funds): Full repatriation allowed for up to two residential properties. Additional properties fall under the USD 1 million per financial year limit from NRO account.

- If bought with Indian rupees or from NRO account (or inherited): Repatriation capped at USD 1 million per financial year (April-March) from NRO account, regardless of number of properties.

- Agricultural land, farmhouses, or plantations generally cannot be repatriated freely.

You need a Chartered Accountant’s certificate in prescribed format, Form 15CA/CB, and proof of tax payment. In one Singapore-based client’s case, we repatriated full proceeds of two residential flats bought with NRE funds without hitting the $1M cap. But for a third inherited property, we routed through the annual limit after proper documentation.

Plan your sales carefully — staggering them across financial years can help maximize repatriation if you exceed limits.

DTAA Benefits – Your Shield Against Double Taxation in NRI Tax Implications

India has Double Taxation Avoidance Agreements with over 90 countries. You can claim lower withholding rates on rental income, interest, or capital gains and get credit for Indian taxes paid in your home country. Submit TRC + Form 10F to claim benefits.

Many NRIs from the US or UK overpay TDS at 30% on rent but recover via DTAA and ITR filing. Always explore DTAA in your NRI tax implications checklist — it can reduce effective tax significantly.

Exemptions and Deductions Available to NRIs

You can claim:

- Section 54: Reinvest LTCG in one residential house in India within specified timelines.

- Section 54EC: Invest in specified bonds (NHAI, REC etc.) up to ₹50 lakhs within 6 months.

- Standard deductions on rental income and home loan interest (subject to conditions).

These exemptions form an important part of smart NRI tax implications planning and can bring your tax bill down substantially.

Filing ITR and Compliance Tips for NRIs

File ITR-2 or ITR-3 (depending on income sources) by the due date (usually July 31 for non-audit cases). Report all Indian income, claim DTAA benefits, and apply for refunds. Keep PAN active and linked to your bank accounts.

A common mistake I see: NRIs assuming “no tax liability after TDS” and skipping ITR. This blocks refunds and creates issues during future repatriation or loans.

Conclusion: Plan Your NRI Tax Implications Early for Stress-Free Ownership

NRI tax implications on property cover purchase costs, rental TDS, capital gains on sale, repatriation limits, and DTAA relief. With Budget 2026 simplifying TDS compliance (no TAN needed from Oct 2026), the process is becoming smoother, but careful planning remains essential.

Treat taxes and FEMA as your allies, not obstacles. Consult a seasoned property advocate and chartered accountant familiar with NRI matters before any transaction. Document everything properly, claim all eligible benefits, and you can enjoy your Indian property investment with full peace of mind — whether for personal use, rental income, or future sale.

Your foreign earnings deserve secure growth back home. Follow these NRI tax implications diligently and make your real estate journey rewarding.

Tags:

NRI tax implications on property purchase and sale India 2026, TDS on property sale by NRI Budget 2026 changes, capital gains tax for NRIs on property sale India, repatriation of property sale proceeds for NRIs FEMA rules, DTAA benefits for NRI rental income and capital gains,

NRI home loan tax implications and deductions, rental income TDS rate for NRI property owners, Budget 2026 TAN removal for NRI property transactions, how NRIs can claim refund of excess TDS on property, long term capital gains tax rate for NRIs 12.5% vs 20%, documents for NRI property sale tax compliance India, avoiding double taxation on Indian property for NRIs, NRI ITR filing for property income 2026 guide, stamp duty and GST on property purchase by NRI, section 54 exemption for NRI capital gains reinvestment.